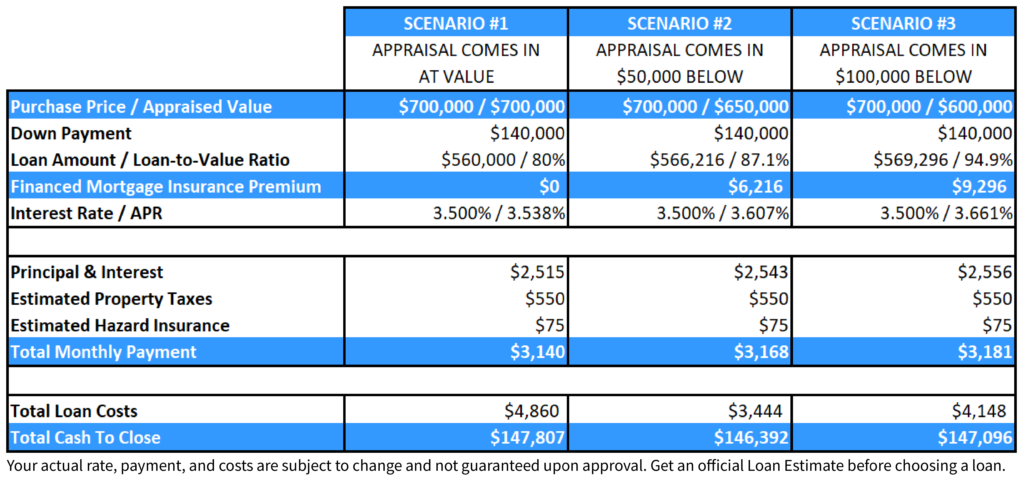

In our competitive housing market, most homes are receiving numerous offers and sell for over the listing price. But what happens when the home appraises for less than its selling price? In a seller’s market, it’s often left to the buyer to cover the difference between the purchase price and the appraisal. And what happens if an appraisal comes in short by $50,000? Or even $100,000? If the borrower does not have extra funds to cover the appraisal gap, Homeseed has a back up plan to help your borrower save the deal.

A scenario we’ll use to go over our appraisal gap strategy is a purchase price of $700,000 with a 20% down payment. If the appraised value comes in $50,000 or $100,000 below the $700,000 purchase price, our loan to value ratio will increase above 80% and the borrower will be required to purchase a mortgage insurance policy. What we can then do is finance a single-premium mortgage insurance policy into the loan amount that helps us cover the appraisal gap. This also allows us to keep the required cash to close similar across all three scenarios. Financing the mortgage insurance premium will increase the loan amount and thus the monthly payment, but not by much. On a $50,000 short appraisal value, monthly payment only increases by about $28. On a $100,000 short appraisal value, monthly payment increases by about $41. This is a relatively inexpensive way to cover up a large appraisal gap in this market.

Please reach out if you’d like to learn more about this financing strategy and other ways to help you clients remain competitive in this market. If you also have anyone looking to get pre-approved to purchase a home or refinance, we’d love the opportunity to serve them!